HAVERTY FURNITURE COMPANIES (HVT)·Q4 2025 Earnings Summary

Havertys Q4 2025: Revenue Up 9.5% as Furniture Retailer Posts Second Straight Quarter of Growth

February 24, 2026 · by Fintool AI Agent

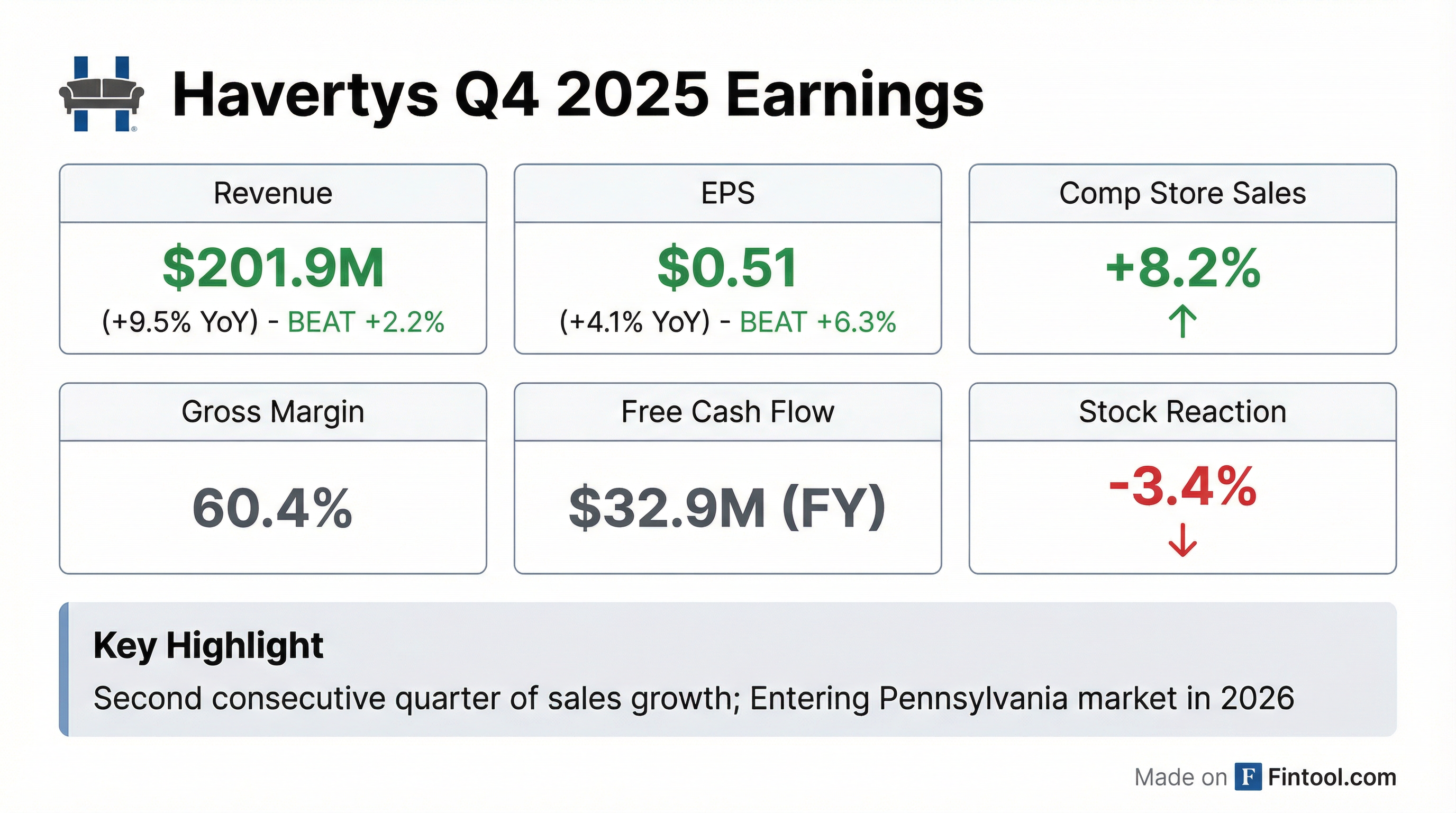

Havertys (HVT) reported Q4 2025 results that topped estimates on both revenue and EPS, delivering its second consecutive quarter of sales growth despite persistent headwinds in the furniture industry. Revenue rose 9.5% year-over-year to $201.9 million, with comparable store sales up 8.2% . Diluted EPS came in at $0.51, up from $0.49 a year ago .

The stock fell 3.4% on the day of the release, closing at $25.30—a reaction that may reflect margin compression and tariff uncertainty rather than the top-line beat.

Did Havertys Beat Earnings?

Yes—Havertys beat on both metrics:

This marks seven consecutive quarters of EPS beats for Havertys, though the magnitude has varied significantly. The company's design-focused strategy and marketing investments continue to drive traffic and increase average tickets. Design business accounted for 33.3% of Q4 sales with average ticket of $8,072 .

What Changed From Last Quarter?

Momentum continued. Q4 marked the second consecutive quarter of growth in both written and delivered sales after a challenging period in early 2025:

Monthly trends showed divergence. CFO Richard Hare provided intra-quarter detail on the earnings call :

The delivered sales strength in December reflected backlog conversion, while written sales weakened after a strong October—a pattern management attributed partly to the 45-day government shutdown impacting consumer confidence .

Design consultants drove higher tickets. Design consultants accounted for 33.3% of written business in Q4 . Average design ticket reached $8,072, up 11.9% year-over-year, with pieces per ticket also increasing . After Thanksgiving sales were up 6.2% with design average tickets of ~$8,500 .

LIFO headwinds hit margins. Gross margin declined 150 bps year-over-year to 60.4%, primarily due to $3.9M in LIFO charges (compared to a $925K LIFO pickup last year) . Excluding LIFO, gross margin actually improved to 62.4% from 61.4% .

How Did the Stock React?

Despite beating estimates, HVT shares fell 3.4% on the day:

The sell-off likely reflects:

- Margin pressure from tariff-related LIFO adjustments

- Tariff uncertainty following Supreme Court ruling

- Weak written sales growth of only +3.5% (vs +9.5% delivered)

What Did Management Guide?

Havertys provided 2026 guidance with a notable caveat around tariffs:

The tariff wildcard: On February 20, 2026, the Supreme Court ruled the IEEPA tariffs were illegal . As of 12:01 AM today (February 24), a 10% worldwide tariff under Section 122 of the 1974 Trade Act replaced the IEEPA and fentanyl tariffs . Key details:

- Section 122 tariffs are not stackable with Section 232 tariffs or USMCA

- Are stackable with Section 301 tariffs

- Section 232 upholstered wood furniture tariff remains at 25% (additional 5% delayed)

- Section 122 tariffs expire in 150 days (July 24)

CEO Burdette emphasized the company will be "thoughtful and deliberate" in responding: "Our current inventories already have the tariffs baked in them, so we've got to work through those inventories... there's not gonna be any actions or reaction off of it. We're gonna wait and see how it plays out over the next few months."

What's the Growth Strategy?

Havertys is doubling down on geographic expansion while refreshing its existing fleet:

New store openings for 2026:

- Pittsburgh, PA (North Pittsburgh) — Across from Ross Township Mall, opening Q4 — first store in Pennsylvania, the company's 18th state

- St. Louis — announced

- Nashville — announced

- Houston (2 locations) — announced

- Additional locations in lease negotiations

Store closures: Alexandria, LA location closing in March after 40+ years due to demographic shifts, stagnant housing growth, and need for major remodel .

Remodels and refreshes:

- 4 full remodels planned

- Mattress and design area refresh covering ~35% of stores in 2026

- All new stores served by existing distribution network (no new investment needed)

CapEx breakdown for 2026 ($33.5M total) :

- New/replacement stores, remodels, expansions: $27.2M

- Distribution network: $3.2M

- Information technology: $3.1M

CEO Burdette emphasized the company's strategic foundation: "Our debt-free balance sheet, our Havertys-branded products, our operational consistency, our integrity, our consumer focus, our design services, our commitment to quality, and our regret-free experience provides our customers with the comfort and confidence to know that furnishing their homes with Havertys is a great long-term investment."

Balance Sheet and Capital Returns

Havertys maintains a fortress balance sheet:

Shareholder returns in 2025:

- Dividends: $20.8M ($5.3M in Q4)

- Share Repurchases: $4.8M (216,482 shares at avg $22.63)

- Q4 buybacks: $2.8M at avg $22.63

- Total: $25.6M returned to shareholders

New authorization: On February 20, 2026, the Board approved an additional $15 million for stock repurchases, bringing total availability to approximately $18.3M .

Full Year 2025 Results

Q&A Highlights

On tariff inventory positioning: Havertys pre-loaded inventory in Q4 to get ahead of tariffs. Inventory was up $12.7M year-over-year to $96.2M . Management expects inventories to decline over the next six months as they work through existing stock .

On gross margin guidance confidence: Even if tariffs increase to 15% from 10%, CFO Hare confirmed margin guidance of 60.5%-61% remains unchanged . Key drivers: prices stabilizing means less LIFO pressure in 2026; gross margins are guided higher than 2025 despite tariff uncertainty .

On variable SG&A outlook: Variable SG&A expected at 18.6%-18.8% (flat with 2025) despite sales leverage. Higher selling costs from sales commissions and potential third-party credit costs offset leverage gains . Fixed/discretionary SG&A rising ~$10M to $307-309M, with ~40% from occupancy costs and rest from wage/benefit inflation .

On mattress program traction: Management highlighted success of mattress department refresh: "It's easier for the consumer to understand what they're looking at... I think calling out the brands has certainly helped attract consumer attention." While industry mattress sales were down mid-single digits in Q4, Havertys was flat—outperforming peers .

On marketing spend: Marketing spend increased ~$4M in 2025 (after cutting too much in 2024). Expected flat in 2026 . Direct mail campaign in late October (16 pages, 750K new customers) with refined targeting and pricing drove improved conversion .

Key Risks and Concerns

-

Tariff uncertainty remains the biggest overhang. Section 122 tariffs expire July 24 and the administration is "aggressively looking at other alternatives under Section 232, Section 301" . The furniture import chain remains exposed.

-

Written sales decelerated sharply. October written sales were up high single digits, but December was down low single digits . Management attributed this partly to the government shutdown creating "unknowns" .

-

Conversion rates slightly down for the quarter despite traffic improvement . Converting store visitors remains a challenge.

-

Inventory build-up. Inventories up $12.7M (15%) to get ahead of tariffs . If consumer demand softens, this could pressure working capital.

-

Credit cost pressure. 60-month financing offers increased credit costs in Q4 to remain competitive . May persist in 2026 .

The Bottom Line

Havertys delivered a solid Q4 with revenue and EPS beats, momentum in comp sales, and an aggressive growth plan for 2026. The debt-free balance sheet and consistent shareholder returns provide downside protection. However, tariff uncertainty, margin pressure, and the gap between written and delivered sales warrant monitoring.

For a $412M market cap company trading at roughly 21x trailing earnings ($1.19 EPS), the risk/reward hinges on whether Havertys can sustain its comp sales momentum while navigating the tariff environment.

View the full Q4 2025 earnings document or explore more about Havertys.